To market, to market...

Various events, including shareholder buy-ins or buy-outs, acquisitions of successful start-ups by large investor companies, and the gifting of shares to family members (and other estate planning) can make it necessary to obtain a valuation of the shares in a private company.

Share valuations have come under increased scrutiny from the Revenue Commissioners in recent years, and third-party valuation advice is being sought for the purposes of supporting the values that are being attributed to shares when share transfers happen.

Revenue acknowledges that valuation is not an exact science, but it is not to be inferred that any value could be defended as the market value of an asset.

Criteria to be considered

Documentation of the facts and assumptions supporting the selection and application of appropriate valuation methods is paramount. Various criteria should be considered by the valuer with regard to the selection of appropriate methods, including:

- The nature of the company being valued,

- The nuances of the industry within which the company operates,

- The life-cycle stage of the company,

- Whether the company is profitable,

- The size of the shareholding being valued,

- Whether the company is highly leveraged,

- The forecast performance of the company over an appropriate time period, and

- The jurisdictions the company is operating within.

Traditional valuation methods are not easily applied to many typical 21st century share-valuation scenarios.

Take, for example, the valuation of an early-stage company in a loss-making position, with intangible assets such as intellectual property, but without any significant tangible assets; or the valuation of a company operating in the technology sector – a sector in which companies either do incredibly well or go quickly bankrupt with unreliable forecast information.

The increased complexity in valuing such companies demonstrates the importance of engaging a valuation specialist to produce an objective and robust valuation report where a share transfer event is being considered.

Tax obligations

In the context of this article, it is informative to consider at a high level the Irish capital gains tax (CGT) and Irish stamp-duty position with regard to the calculation of market value.

Share transactions can give rise to various tax obligations, depending on the circumstances of the transaction, but CGT and stamp duty arise most frequently.

Irish CGT legislation does not prescribe the basis of valuation. The valuation rules for Irish CGT purposes are set out in sections 547-549 of the Taxes Consolidation Act 1997 (TCA).

Section 548 provides that the market value in relation to any assets means the price that those assets might reasonably be expected to fetch on a sale in the open market.

Valuation rules

The valuation rules for Irish stamp duty purposes are contained in section 19 of the Stamp Duty Consolidation Act 1999 and import the valuation method contained in section 26 of the Capital Acquisitions Tax Consolidation Act 2003 (CATCA).

Section 19 provides as follows: “The commissioners shall ascertain the value of property the subject of an instrument chargeable with stamp duty in the same manner, subject to any necessary modification, as is provided for in section 26 of the Capital Acquisitions Tax Consolidation Act 2003.”

Section 26 CATCA provides that, when valuing shares in an unquoted company, the shares passing must be valued on the basis of a hypothetical sale in a hypothetical open market, between a hypothetical willing vendor and a hypothetical willing purchaser.

The price cannot be reduced by reason of the whole of the property being placed on the market at the same time. It must be assumed that the purchaser has all information available that a prudent purchaser might reasonably require.

Market-value concepts

On the basis that general market-value principles apply for Irish CGT and Irish stamp-duty purposes, the valuation obtained for the purposes of these taxes should be the same.

A detailed review of market-value concepts in respect of all Irish tax heads is beyond the scope of this article, but it is worth noting that section 27 CATCA 2003 prescribes strict rules for the purposes of valuing certain shares in private companies.

Essentially, the section outlines that, where a successor or donee, together with his/her relatives, nominees and trustees, control the company, the value of the shares received by that donee/successor must be valued as a proportionate part of the value of the company as a whole.

This section is particularly controversial in light of the fact that the principal consequence is to disallow discounts for minority shareholdings when valuing shares in a controlled private company.

Accordingly, the shares being valued may be worth less from a commercial perspective than the value imposed from a CAT perspective.

Valuation approaches

There are a number of generally accepted approaches to ascertaining the fair market value of the shares of a private company. The following valuation approaches are accepted by most tax administrations, and are consistent with generally accepted accounting principles in most jurisdictions.

1. Prior sales/offers

One of the most defensible valuation techniques available for the purposes of valuing shares in a private company is the identification of recent arm’s-length sales of shares or offers to purchase shares in (a) the company being valued or (b) in a comparable company.

In this regard, it is important to bear in mind that Revenue is unlikely to accept a valuation that is lower than the value that a willing buyer has demonstrated they will pay for the same or similar shares in the absence of significant evidence of different/updated circumstances.

In practice, previous arm’s-length share sales are likely to be uncommon in the context of an unquoted company.

Additionally, information may not be readily available concerning sales of shares in comparable unquoted companies, or it may not be possible to identify appropriate comparable companies.

At a high level, the following characteristics are often considered when establishing whether one company is comparable to another company:

- Industry sector,

- Market position,

- Geography,

- Stage in life cycle of the business,

- Growth rate,

- Size,

- Profitability, and

- Capital structure.

Where prior sales/offers information is available, the background circumstances pertaining to such previous offer/share sale will be important in order to determine the significance of that information in the context of the current valuation being undertaken – for example, whether a minority/majority holding was being sold at the time, what class of shares were being sold, what rights were attached to the shares being sold, etc.

2. Earnings-based approach

In general, an earnings-based approach is most appropriate for the valuation of a majority shareholding in a company that is a going concern (that is, a business that is expected to continue to operate for the foreseeable future).

The earnings-based method is recognised by the Irish tax authorities as the method normally used to value trading and manufacturing companies.

This approach involves identifying the ‘maintainable earnings’ of the company, and the maintainable earnings are then capitalised using an appropriate multiple in order to produce a valuation.

The most recent set of audited accounts is a common starting point for the calculation of the maintainable-earnings figure, but where profits are erratic, it may be more representative to use a weighted average of, say, the past five years of audited results.

In order to calculate a representative and normalised maintainable-earnings figure, the valuer will often use earnings before interest, tax, depreciation and amortisation (EBITDA) as a starting point.

The EBITDA is then adjusted to remove the effect of non-recurring items, and the valuer must consider whether each income stream is expected to continue into the future.

Similarly, costs should be reviewed to establish whether they are expected to be incurred at the same level in the future, and whether there are any additional costs that are likely to arise on an ongoing basis.

It is also worth noting that maintainable earnings generally refer to net-of-tax profits, as adjusted for the items that have just been mentioned, but for small- and medium-sized companies, it is common for maintainable earnings to be calculated on a pre-tax basis.

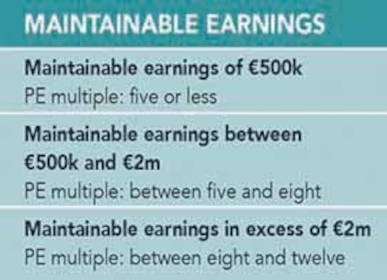

The price/earnings (PE) ratio is the most common multiple used for the purposes of applying the earnings-based approach. At a basic level, the valuer should undertake market research to identify a quoted company/companies with similar underlying characteristics to the company being valued.

When a suitable quoted company has been selected, the normal practice is to multiply the price earnings ratio appropriate to the quoted company (or average price earnings ratio applicable to the comparable companies), less a discount to compensate for the lack of marketability of the shares of a private company, by the future maintainable earnings of the company being valued.

Des Peelo, a well-known author in the area of share valuations in Ireland, suggests the following PE multiples as a rough guide for valuing Irish companies in his book, The Valuation of Businesses and Shares:

3. Income-based approach

The income approach is predicated on the idea that the value of the equity of a company is the present value of the future distributable reserves of that company. The discounted cash-flow (DCF) method is the most popular application of the income approach.

The DCF method involves estimating the amount and timing of the future cash flows of the company over an appropriate period.

An appropriate discount rate must then be applied to the cash flows that are identified, reflecting a rate of return on investments appropriate to (a) the company being valued and (b) the relevant market conditions. The total of the discounted cash flows is the value of the company.

The DCF method should involve a rigorous review of projected performance, and is often preferred as a valuation method where credible financial data is available. It is often the case that management teams are not in a position to forecast with any degree of reliability, due to the unpredictable nature of the industry in which they operate (for example, in the case of a technology company).

In such circumstances, the DCF method is unlikely to be appropriate. In particular, the calculation of some of the components of the DCF calculation (for example, the ‘weighted average cost of capital’, if applied as the discount factor) can appear mathematically complex, which may provide unmerited comfort with regard to the accuracy of the valuation.

As such, it is important to bear in mind that the valuation obtained using this technique is only as reliable as the information used to calculate it.

4. Asset-based approach

The asset-based method involves adjusting all assets and liabilities (including off balance-sheet, intangible, and contingent assets and liabilities) to their fair market, current values.

This method is not normally satisfactory when applied in isolation in the context of a company that is a going concern. However, in our experience, this method can provide indicative valuations in the following situations:

- Companies operating in capital intensive industries (for example, real estate companies),

- No earnings history, and

- No consistent, predictable customer base.

Minority shareholdings

In most cases where a minority shareholder wishes to sell their shareholding in a company, a discount will be applied to reflect the fact that the shareholding does not represent a majority (and, therefore, does not enable the owner to control the company).

In general, the following table, as identified by Peelo (p64 of the aforementioned book), represents the appropriate discount rates to apply when valuing minority shareholdings:

However, there are certain circumstances where the valuer must exercise judgement as to the appropriate discount to apply in respect of a minority shareholding.

For example, a minority shareholding may be part of a possible combined majority shareholding with a spread of 40%:40%:20%. Other factors that may increase or decrease the discount include circumstances where there are additional rights attaching to the shares.

Established discounts

In a recent determination (specifically in paragraph 42, 12TACD2017), the Tax Appeals Commissioner (TAC) outlined how he was persuaded by the coherent analysis put forward by the expert witness on behalf of the respondent in selecting an appropriate minority shareholding discount, by reference to the table listed above and another similar table contained in a book called Valuation of Shares in Unlisted Companies for Tax Purposes, by Denis Cremins.

In this regard, the TAC acknowledged that these tables represent “an established range of discounts for lack of control and marketability in minority shareholdings”. This is significant because, while determinations by the TAC are not binding on other courts, they have considerable persuasive effect.

Another issue, related to company share sales (which generally requires a valuation exercise to be undertaken), is the existence of contingent or unascertainable consideration in the form of an earn-out.

We will address this topic in a follow-up article.