Crash test dummies

Irish PI awards are only around 1.55 (not 4.4) times British awards

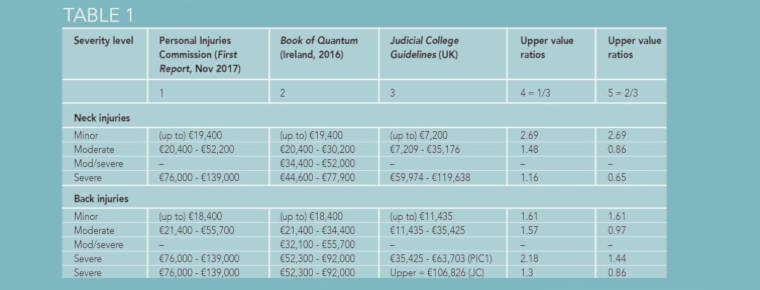

The Personal Injuries Commission’s first report (PIC1) in 2017 compared general damage guidelines for minor, moderate, and severe neck and back injuries in the Irish Book of Quantum 2016 to those in Britain’s Judicial College Guidelines.

Table 1 reproduces its results. PIC1 concluded: “At a cursory level, this indicates that less severe injuries in Ireland tend to attract higher levels of damages, but that is less pronounced as the severity of injury increases.”

It is safer, however, to conclude that minor injuries tend to attract higher upper guideline damages in Ireland, but tend to attract lower upper guideline damages as the level of severity increases. The reasons for this qualification are:

- The PIC overstates some Quantum guideline values. For example, PIC1 gives €76,000 to €139,000 as the guideline range for both ‘severe’ neck and ‘severe’ back injuries, whereas the Book of Quantum gives €44,600 to €77,900 as the guideline range for ‘severe’ neck injuries.

- The Quantum upper guideline value for ‘severe’ neck injury in Ireland of €77,900 is just 65% of the British upper guideline of €119,638. Consequently, the Irish upper guideline is 35% lower (not 16% higher) than the British upper guideline.

- The PIC classifies ‘moderately severe’ injuries as ‘moderate’ instead of as ‘severe’ injuries. For example, the Quantum ‘moderately severe’ neck injury range is €34,400 to €52,000. If you combine it with the ‘severe’ neck injury range (€44,600 to €77,900), it has no impact on the ‘severe’ €77,900 upper guideline value. However, if you combine it with the ‘moderate’ guideline range, the ‘moderate’ Quantum upper guideline jumps from €30,200 to €52,000. The actual Quantum moderate neck injury upper guideline for Ireland is €30,200 and is 86% of the British upper guideline of €35,176. The Irish upper guideline is 14% lower (not 48% higher) than the British upper guideline.

- The PIC combines different injury categories in ways that may hinder comparison. For example, PIC1 gives €139,000 as the upper guideline value for ‘severe’ back injury, whereas Quantum (p21) gives €92,000 as the upper guideline value. Examination of Quantum (p33) shows that the higher €139,000 PIC1 value, in fact, refers to (severe and multiple) vertebral fractures, whereas the lower Quantum €92,000 (p31) refers to back injuries. PIC1 does not state that it has amalgamated these injury categories, or why it has done so.

Three categories

The 14th edition of the Judicial College Guidelines (with 10% uplift) distinguishes three categories of ‘severe’ back injuries, with upper guideline values of £141,150 (most severe), £77,540 (second most severe), and £61,140 for ‘severe’. These translate to €194,462, €106,826 and €84,232 at the 2015 period-average exchange rates (£0.72585 = €1) or to €159,499, €87,620 and €69,088 at the exchange rate of £1 = €1.13 that PIC1 used.

The Irish Quantum upper guideline value of €92,000 for severe back injury is 86% of the British upper guideline if we take €106,826 as the upper British guideline value for severe back injury.

Complexity

All of the foregoing confirms that comparing awards is complex and benefits from judicial experience and discretion that has due regard to official guidance, medical and technical expertise, and advocacy on behalf of plaintiffs and defendants.

Of course, the system can be improved – for example, by higher frequency and more detailed updates of Quantum. However, in complex cases, the appropriate awards are not formulaic and cannot be read from a table or a book, however useful they may otherwise be.

Actual awards

Ultimately, what matters are not guideline awards but actual awards. The second and final report of the Personal Injuries Commission (PIC2) in July 2018 compared general damages for whiplash injuries in Ireland and Britain. Its key finding (p15) is that “[Irish] soft tissue injury claim costs are approximately 4.4 times that of the UK cost”.

It follows that, if whiplash awards account for 29.4% or more of total motor insurance costs, then, other costs being equal, the total Irish motor insurance cost per whiplash claim are over two times the British cost.

It’s all relative

The number of claims per vehicle year in Ireland is 80.61% of the British claims rate and – if PIC2 is correct – the average total insurance cost per claim in Ireland is over twice (that is >2) the British cost. The product of the relative claims rate (80.61%) and relative total cost per claim (>2) gives the average total cost per vehicle policy year in Ireland vis-à-vis Britain (that is, >1.61).

This implies that, if Irish whiplash awards are 4.4 times British awards, then we should expect that the total Irish insurance cost per policy year will be at least 60% higher than the British cost, and this should also be reflected in Irish motor insurance premiums compared with Britain.

Premium comparisons

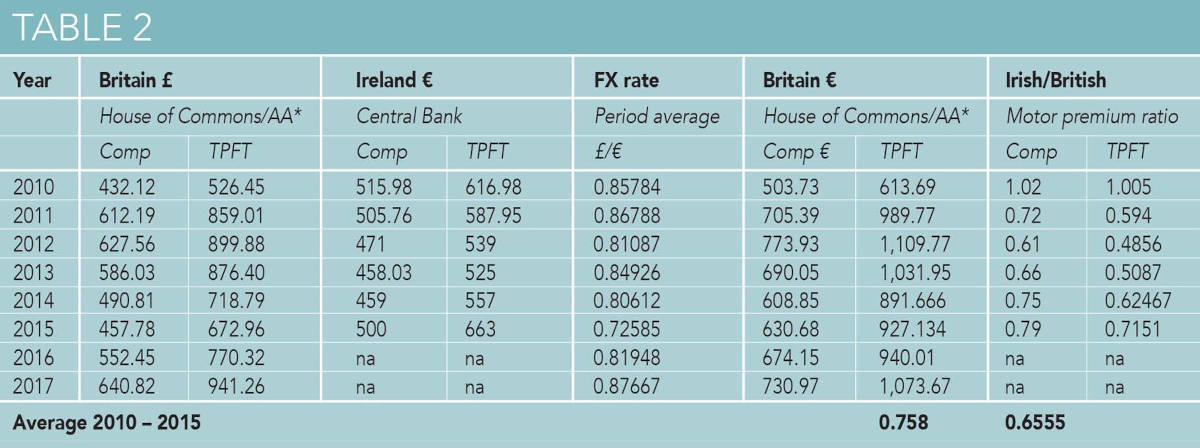

Table 2 compares Irish and British motor insurance premiums between 2010 and 2015. For example, in 2015, the House of Commons/AA-sourced comprehensive British motor premium was Stg £457.78, which translates to €630.68, at the period average exchange rate (£0.72585 = €1). Dividing the 2015 Irish comprehensive premium of €500 by €630.68 gives 0.79, which means that the average Irish comprehensive premium was 21% lower than the average British premium in 2015.

Table 2 shows that, between 2010 and 2015, comprehensive motor premiums in Ireland averaged 24% less than British premiums: Irish third-party fire and theft (TPFT) premiums averaged 34% less than in Britain.

If Irish insurers’ total cost per policy year was at least 60% higher than in Britain, how could Irish insurers offer Irish motorists premiums that were a quarter to one-third less than British premiums between 2010 and 2015?

The Table 2 premium estimates are inexact, but I know of no credible adjustments to them that can reconcile the yawning cost-premium gap set out above. It is more fruitful to re-examine more closely the PIC2 claim that Irish whiplash awards are 4.4 times British awards.

Claims versus injuries

PIC2 (p21) notes: “For each company, an injury code is allocated to claims based on the most dominant or severe injury and is generally set when the claim is first reported.” Hence, a whiplash claim is a claim where the most dominant or severe injury is a whiplash injury.

However, a whiplash claim is not the same as a whiplash injury. As Mark Strang (ISO/Verisk) observes: “On average, there are 2.1 separate injuries per soft-tissue claim.”

Actual payouts

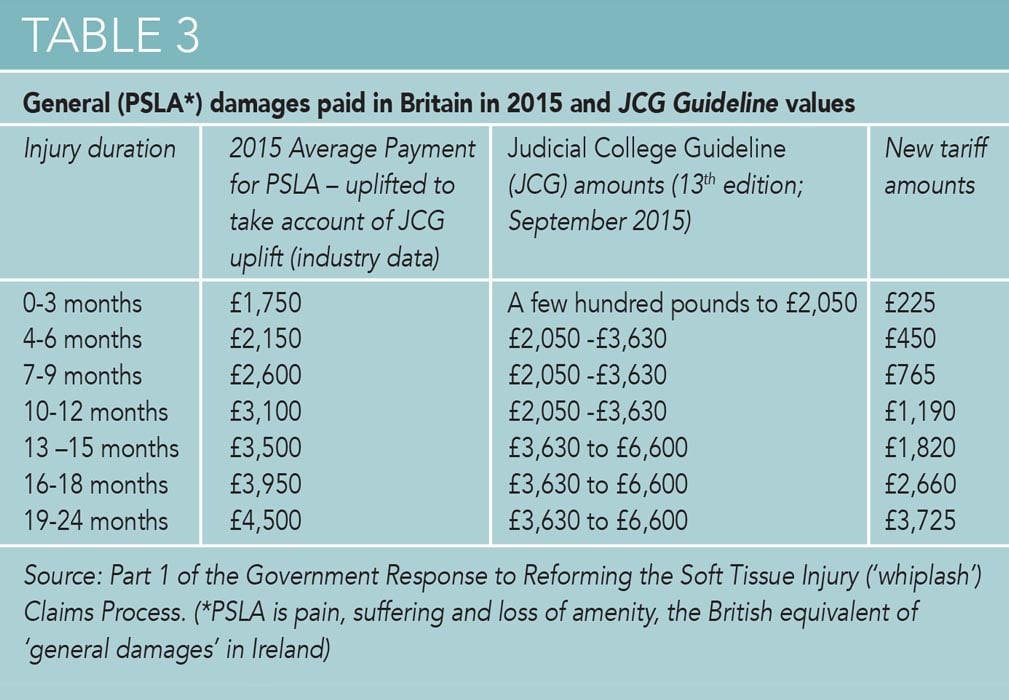

Table 3 gives the British guidelines and actual payouts for a whiplash injury of a given duration in 2015. It is clear that each British award set out in Table 3 refers to a single whiplash injury.

PIC2 estimates the cost of a whiplash claim for Ireland, but it acknowledges (p21) that: “Where a claimant has multiple injuries, the data includes the payment made for all injuries rather than just the soft-tissue injury element. This may result in average costs of soft-tissue injury being overstated.”

In short, PIC2 compares the award for a whiplash injury in Britain with the award for a whiplash claim (circa 3.1 injuries) in Ireland. It is reasonable to expect that the Irish award for all (3.1) injuries in a single Irish whiplash claim will average around twice the award made for just a single whiplash British injury on its own.

Faux pas

The PIC2 methodological faux pas of comparing an Irish whiplash claim award with a British whiplash injury award overstates – by around 100% – the true cost of whiplash injury awards in Ireland compared to Britain. By itself, this means that Irish whiplash awards are not 4.4 times British awards – they are more like 2.2 times British awards.

We could reduce the 2.2 multiplier further by incorporating other factors seriatim, but it is more meaningful to compare personal injury (PI) awards in Ireland and Britain than to compare ‘whiplash’ awards (a) because PI awards are similarly defined and understood in Ireland and Britain, and (b) because, as PIC2 (p21) acknowledges, “the definition of soft tissue injury (‘whiplash’) losses is constantly developing and is not consistent between Irish companies, between Ireland and the UK jurisdiction, and between successive UK soft-tissue analyses.”

Comparative PI awards

In 2015, Irish motor insurers paid PI claimants on average €22,719; British insurers paid PI claimants on average Stg £10,614, which converts to €14,622 at the 2015 period-average exchange rate. The average Irish PI award in 2015 was, therefore, 1.55 (not 4.4) times the average British award.

Awards levels depend, among other things, on injury severity. Between 2008 and 2013, Ireland’s road fatality rate (per registered vehicle) was 47% higher than in Britain. Ireland’s serious injury rate was two to three times the British rate (as measured by clinical assessment of hospital admissions using the MAIS3+ international injury scale). I

estimate that Ireland’s higher injury severity compared with Britain, by itself, increased Ireland’s cost per PI claim to around 1.67

times the British cost.

1.55 (not 4.4)

To summarise, Irish PI awards are around 1.55 (not 4.4) times British awards, and this is almost entirely due to the higher injury severity of Irish accidents compared with Britain.

PI awards make up circa 70% of insurance expenditure, so if non-award PI costs (for example, service delivery, commission, MIBI, etc) are the same in Ireland and Britain, then the total Irish cost per claim is 1.39 times the total British cost.

The Cost of Insurance Working Group reports that the Irish claims rate per vehicle year is 80.61% of the British rate (8,494/10,537). This implies that the total cost per vehicle year in Ireland is 1.12 (that is, 1.33 x 0.8061) times the British cost.

Casualty rate

The garda-reported overall casualty rate per licensed vehicle in Ireland is around 57% of the British rate, and implies that the total cost per licensed vehicle in Ireland is 79% (that is, 1.39 x 0.57) of the British rate. Some licensed vehicles are uninsured but, nonetheless, contribute to Irish motor insurer costs via insurers MIBI (Motor Insurance Bureau of Ireland) contributions.

The actual motor insurance premiums set out in Table 2 give far greater support to the claim that Irish PI awards are 1.55 times the British PI award than to the PIC2 claim that Irish whiplash awards are 4.4 times the British whiplash award.

Insurers’ costs

Also, insurers’ costs show that big (non-whiplash) claims settling above €100,000 increased its share of total Irish claims costs from 11% to 17% between 2010 and 2015, and its share of total claims from 0.2% to 0.4%. These awards are underpinned by higher serious and severe road accidents in Ireland, and they require targeted policy measures to address them.

The key policy implication arising from this analysis is that insurance costs and motor premiums are best reduced by reducing accident frequency, especially the frequency of serious and severe road accidents on Irish roads. Ireland has proportionately fewer reported road casualties than Britain, but has a greater preponderance of serious accidents and fatalities.

Preventing a road accident prevents the full cost it would otherwise entail – and that cost is considerable for serious and severe accidents.

Capping

Capping awards shifts some of the cost burden from the insurer to the insured, but does nothing directly to prevent the accident or to mitigate its cost.

Of course, other factors contribute to Irish insurance costs – uninsured driving, late settlement, higher Irish VAT/VRT rates (50%/60% compared with 20%/30% in Britain) – but it is important to get the policy priorities right. Some Irish costs are deliberately set higher than in Britain – for example, bereavement grants are €13,686 in Britain but have a maximum of €35,000 in Ireland.