'Fatal flaw' in motor cover transparency code

The Central Bank’s new Consumer Protection Code (CPC), which comes into effect this week, sets mandatory rules to ensure firms in the financial industry act fairly and honestly, writes Law Society President Rosemarie Loftus (pictured).

The mandatory obligation to provide clear information is crucial.

It recognises that hoping firms will do the right thing is not a regulatory strategy.

This makes what happened with the Government’s new Motor Insurance Transparency Code even more baffling.

Easy pass

Published earlier this month, as part of the Government’s action plan for insurance reform, the code is voluntary, light-touch and gives insurers an easy pass.

It does more to shield insurers than it does to empower consumers.

Insurers can choose to opt in, if they wish, but they are not obliged to do so.

There are no audits or penalties to enforce compliance. It gets worse.

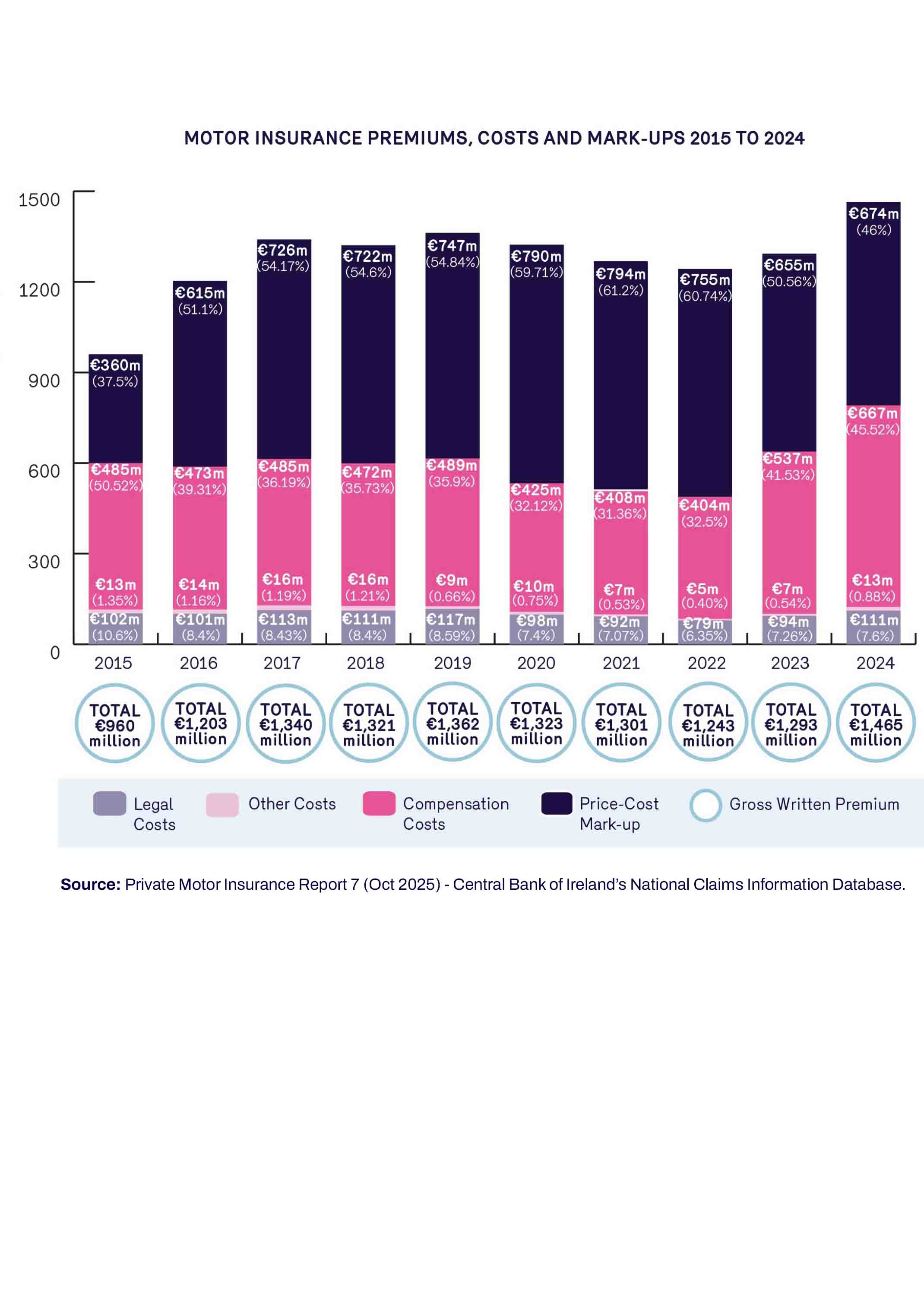

The code fails to meaningfully address the biggest single factor that goes into setting the price of motor insurance premiums, the combined costs and profits of insurers, which is called the ‘price cost mark-up'.

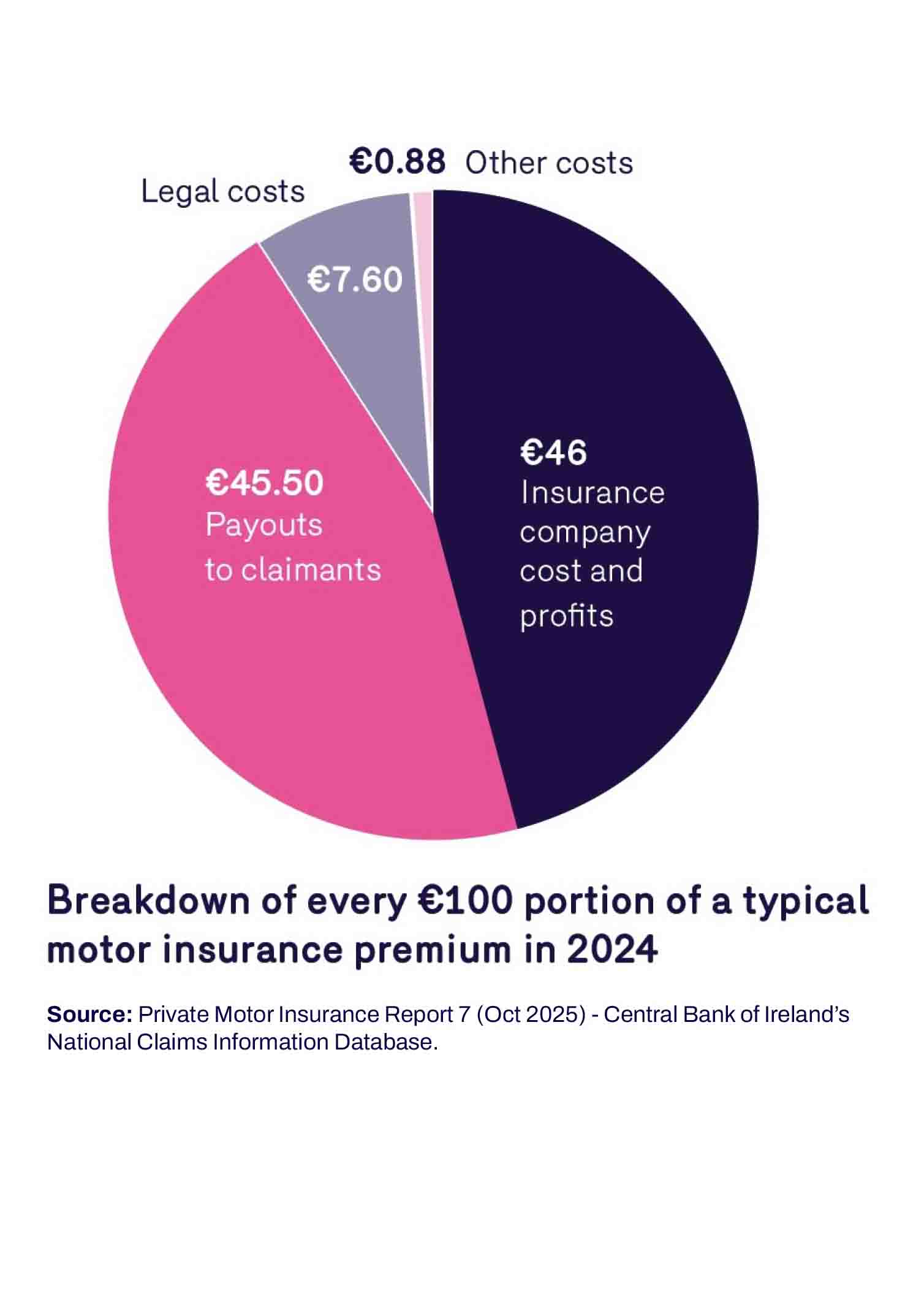

This is a fatal flaw, given that the combined costs and profits of insurers absorb nearly half (46%) of every motor insurance premium paid.

€1.4 billion in premiums

In 2024 a total of €1.4 billion was paid to insurance companies by Irish motorists in premiums.

The Central Bank’s National Claims Information Database shows that for every €100 you pay on your motor insurance a total of €46 was taken up by the costs and profits of the insurer.

For completeness, €45.50 was paid out in claims to those who suffer a loss covered by the insurance, €7.60 covered legal costs and €0.88 covered other costs such as medical costs.

Insurers that volunteer to sign up to the new transparency code are mostly asked to offer tips to drivers on risk mitigation, including “driving behaviour”

There are several pages on 'risk mitigation' for drivers, but just two mentions of insurer profits in what is an 18-page document.

This is risible.

The transparency code needed to be much stronger and more exacting when it comes to insurers’ costs and profits.

For example, the code does not distinguish between reinsurance that an insurer goes out and buys in the marketplace, as against self-reinsurance where an insurer buys reinsurance from itself, or its parent company.

As the Irish Times has already pointed out: Insurers’ reinsurance deals with overseas parents muddy earnings.

Clear picture

Official Central Bank data paints a very clear picture, albeit one that the motor insurance industry has tried to obscure.

Over the past five years, the combined costs and profits of insurers have dwarfed all other elements and have accounted for between 46% and 61% of the total cost to drivers.

In nine out of the last ten years, insurers’ own costs and profits have exceeded the compensation paid out to those involved in motor accidents.

Yet, this is fudged in the new code.

The independent data produced by the Central Bank shows that legal costs averaged 7.9% of motor insurance premiums over the past decade and have fallen as a share of gross premiums – even as overall motor premiums have climbed.

Downward trend

There is a clear downward trend in both accidents and awards.

Road traffic accident claims dropped by 30% between 2019 and 2024, while total award values fell by 41%, according to the Injuries Resolution Board’s May 2025 report.

Despite these savings, premiums rose 9% in 2024 alone.

In spite of the facts, the insurance industry persists in scapegoating legal costs and points the finger of blame at personal injury claims as being the primary drivers of the increased cost of motor insurance.

The insurance industry again tried to scapegoat solicitors and the legal sector for rising costs when welcoming publication of the new Transparency Code.

Even if legal costs were cut by 10%, the premium paid by the average Irish driver would barely budge.

The Central Bank data shows that insurance industry narrative does not hold up to scrutiny.

The reality is that insurers have banked the benefits of a profitable run in the Irish market rather than passing the savings on to consumers.

Point the finger

And insurers continue to point the finger elsewhere when asked why they don’t reduce the cost of motor insurance to consumers.

The sector should be challenged on the data that is available and published by the Central Bank.

Sustained high profits amid falling claims show consumers aren’t sharing in the efficiency gains, despite the Government’s best efforts.

While a profitable and sustainable insurance market is necessary for a healthy economy, consumers deserve to know what they’re paying for – and why premiums keep increasing.

Consumers deserve to have full transparency.

This is essential to counter deflection and build a fairer system.

The lack of transparency around rising motor insurance premiums has long been a source of frustration for every driver in the country.

Over the next 12 months, as renewal notices land, some consumers will see whether insurers who volunteer to sign up to the new Motor Insurance Transparency Code provide meaningful breakdowns.

I won’t hold my breath.

Being half-transparent in any other walk of life is called many things, but you can’t hope to deliver a solution when you ignore half of the problem.

- Rosemarie Loftus is President of the Law Society of Ireland