A second bite at the cherry

In Ireland, the legacy of unsustainable personal debt led to the introduction of the Personal Insolvency Act 2012 (amended in 2015) and the establishment of the Insolvency Service of Ireland (ISI) in 2013.

This realignment of policy has brought about a radical and innovatory approach to the treatment of personal debt, insolvency, and bankruptcy in Ireland.

The act created a number of debt solutions for personal insolvency, in addition to the option that already existed – bankruptcy – and merged the Office of the Official Assignee, which dealt with bankruptcy, into the newly formed ISI.

Despite the initial slow take-up, the ISI has, to date, returned nearly 8,000 debtors to solvency, accounting for almost €10 billion of debt.

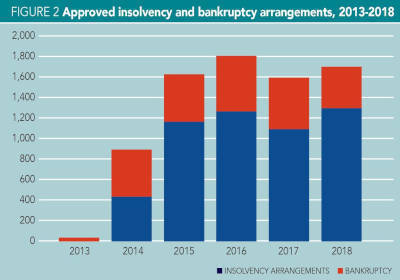

Figure 2 (below) shows that, since its inception, the number of people availing of the debt solutions available through the ISI has grown significantly.

Furthermore, the very existence of prescribed legislative solutions for personal insolvency has acted as a catalyst for credit institutions to directly enter into over 120,000 informal alternative repayment arrangements with debtors.

Personal Insolvency Arrangements (PIAs), the solution that deals with mortgage debt and that aims to keep the debtor in their family home, is by far the most-used solution, accounting for 40% of the total solutions sought.

Most popular restructures

More specifically, with regard to mortgage debt, research undertaken by the ISI found that the three most popular restructures put in place by practitioners as part of a PIA are split mortgage, term extension, and principal reduction.

The average principal reduction per family home is approximately €120,000 and 95% of those entering a PIA remained in their home (based on a representative sample from Q3 2017).

A key aspect of the act is that a debtor is afforded the same protections and opportunity to avail of an insolvency solution, irrespective of the type of creditor to whom they owe moneys (whether the creditor is a main pillar bank, investment fund, credit union, utility company, etc).

This is a key benefit of the new regime for debtors and for any third party advising them in the context of ongoing loan sales to investment funds, or so-called ‘vulture funds’.

Settling in

The initial slow take-up reflected the simple reality that the introduction of such a radical new regime takes time to settle. Debtors were unaware of the extent of the help that was available.

The main credit institutions were initially worried about moral hazard and strategic default, and were slow to engage with the new regime.

As a result, the ISI has been busy working with stakeholders to clear any blockages. Information events and advertising campaigns have been organised to increase debtor awareness.

The ISI has worked closely with credit institutions to emphasise the benefits and financial returns that can be realised from dealing with personal debt in a structured way using the arrangements outlined above.

Working together

The credit institutions, their representative bodies, along with debtor advocates, personal insolvency practitioners (PIPs), and the Courts Service are now working together under the chairmanship of the ISI on the Consultative Forum, the Protocol Oversight Committee, and the Protective Certificate (PC) Target Timeline Group.

The shared aim is to develop a more effective, timely and legally certain personal insolvency process for the benefit of all stakeholders.

An example of this common endeavour is the support of all stakeholders with the ISI’s proposal to Government that Debt Relief Notices (DRNs), Debt Settlement Arrangements (DSAs), PIAs and PCs should be approved by the ISI rather than requiring a court to make an order for their approval.

This would lead to an increase in the accessibility to the personal insolvency system, time and cost savings, and a greater consistency of approach.

Policy developments

Since 2012, the personal insolvency regime has continued to develop and evolve, with a particular emphasis on ensuring that debtors are given every chance to remain in possession of their family home. The more important developments include:

- The introduction of ISI guidelines on reasonable living expenses (a debtor who enters an insolvency solution is entitled to a reasonable standard of living that meets their physical, psychological and social needs),

- The agreement of DSA and PIA protocols with all relevant stakeholders that make it easier for a debtor to reach agreement with his or her creditors through a DSA or PIA (a protocol-compliant arrangement uses agreed documentation, standard terms and conditions, and adheres to high-level principles set out within it),

- Amendments to the legislation reducing the bankruptcy term to one year, and

- Amendments permitting a debtor to seek a court review, in certain circumstances, where creditors reject a PIA – the removal of the so called ‘bank veto’.

The latter are commonly referred to as ‘section 115A reviews’. The ability to seek a 115A review negates the option of the creditor simply vetoing the proposed PIA and increases the likelihood of a PIA proposal being accepted.

Improved understanding

A large number of 115A cases are now progressing through the courts, with the outcomes leading to improved understanding of the obligations and requirements for both debtors and creditors.

Over 1,100 section 115A cases have been initiated in either the Circuit or High Court since 2015 – 400 of these cases have been decided with a 60/40 split in terms of those reviews that have been dismissed (that is, decided in favour of the creditor), and those that have been approved (in favour of the debtor).

Abhaile

The introduction of the Abhaile Mortgage Arrears Resolution Service in 2016 means that a debtor can secure the services of a PIP for free. A number of government agencies are involved, including MABS, the Legal Aid Board, the ISI, and the Citizens’ Information Board.

The scheme is coordinated by the Department of Justice and the Department of Social Protection.

Furthermore Abhaile, with the assistance of the Legal Aid Board, is funding a solicitors’ panel that has been created to provide legal aid to debtors, to allow them bring section 115A cases to court.

The evolution of the personal insolvency process continues and, in 2017, the department issued a consultation process under section 141 of the act asking for suggestions on how to improve the legislation.

The ISI made a comprehensive submission (available on www.isi.gov.ie) and is awaiting the outcome of the department’s deliberative process.

Future challenges

Economic circumstances have changed dramatically in recent years. The prolonged recession has been replaced by a domestic economy that has returned to growth, with increasing employment opportunities, growing income levels, and rising property prices.

While welcome, these favourable economic conditions pose a number of important challenges for the personal insolvency regime and, more importantly, for the return to solvency for those tens of thousands of households that continue to find themselves in deep mortgage arrears.

The emergent return to positive equity of the family homes for this cohort is of particular concern, as it may reduce the restructuring options available, including debt write-down, while masking the underlying issue of affordability.

Improving conditions

The reappearance of more normal economic conditions will also mean increasing interest rates in the medium term from historic lows, and this is likely to have a significant effect on those debtors just on the margin of meeting their financial commitments.

Improving conditions will, in turn, perhaps reduce the focus on the difficulties faced by those who remain indebted and may make it increasingly difficult for those debtors to remain in their family homes as creditors seek to recover a more valuable security.

Arguably, the need for the ISI and the suite of insolvency solutions it provides are more important in these circumstances, where debt restructuring will lead to a second chance with greater opportunities for debtors.

The ISI would encourage you to direct any debtor who might come to you with debt problems to make contact with the ISI, either through the website www.backontrack.ie or through the information line at 076 106 4200, or to direct them to a PIP (their contact numbers are on the ISI and BackOnTrack websites).

Representatives of the ISI are happy to provide information booklets on the statutory solutions available. The ISI is happy to address your staff and colleagues, through information sessions, either locally or regionally.